I Earned Very Little. Should I File a Return? The 2026 Answer Might Surprise You

If you earned a little cash from a side hustle or part-time job this year, you might think you don’t need to file taxes in Canada 2026—but skipping this step could mean leaving hundreds of dollars in unclaimed benefits on the table. Filing your return is the only way to unlock the GST/HST credit, access Alberta family benefits, and build the contribution room you need for your financial future.

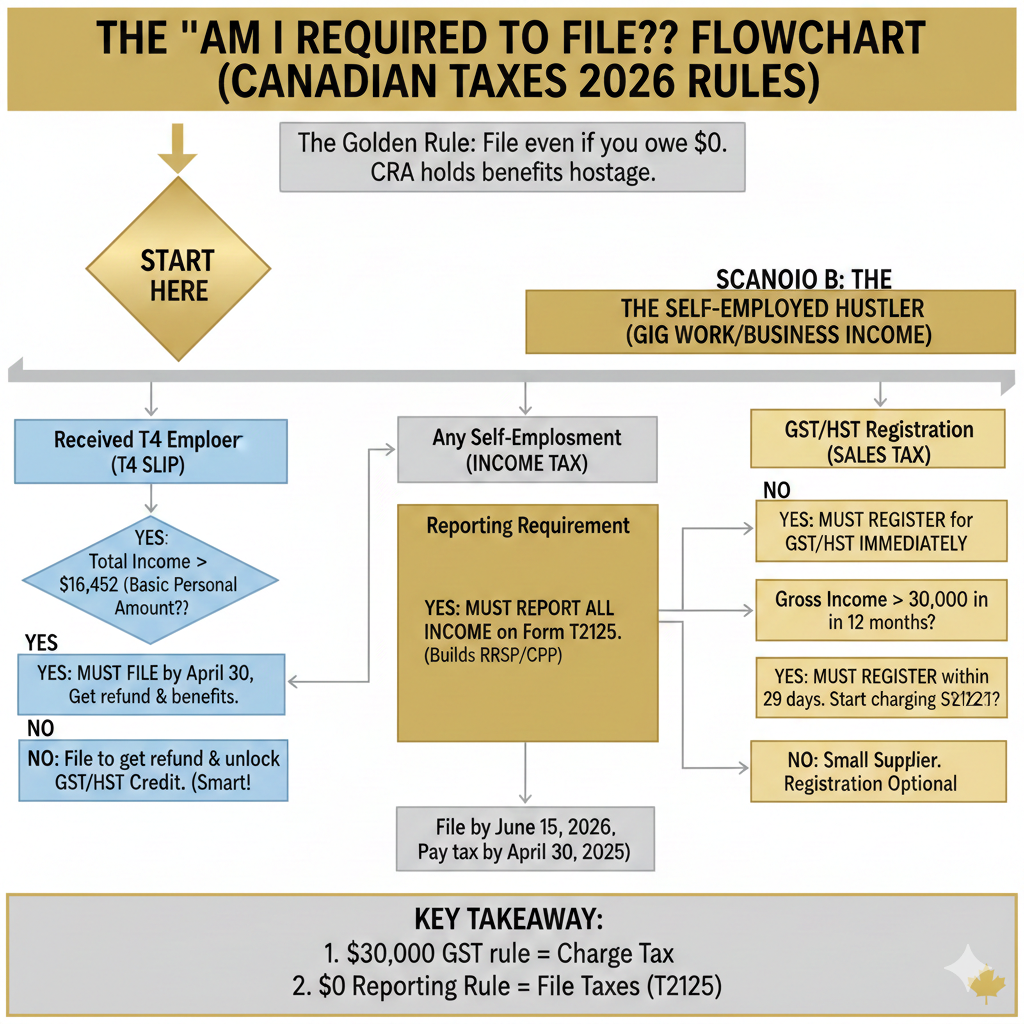

“Am I Required to File?”(The 2026 Rules)

The Golden Rule: Even if you owe $0, you should still file taxes in Canada 2026. The CRA does not release benefits until you file. Here is when you legally must file:

Scenario A: The Employee (T4 Slip)

If you earned money from an employer, taxes were likely deducted from your pay. You need to file to get that money back.

The mandatory filing threshold is generally based on the Basic Personal Amount ($16,452 for 2026). However, filing even when you earn less is a smart financial decision. It triggers the GST/HST credit payments automatically.

Scenario B: Self-Employment and the $30,000 GST Threshold

This part is critical for Calgarians with side income. The rules change based on how much you made:

- Income under $30,000: You do not need to register for a GST/HST number. The only exceptions are taxi and ride-sharing services—they must register immediately.

- Income over $30,000: You must register within 29 days of hitting that threshold. You also start charging tax on your services.

- Reporting Requirement: Here is the non-negotiable part: any self-employment income—even $500—must be reported using Form T2125. The CRA expects to see it, regardless of whether you received a slip.

Key Takeaway: The $30,000 GST rule determines if you charge tax. The $0 reporting rule determines if you file taxes. You must always report self-employment income using T2125, even if you never registered for a GST number. This builds your RRSP contribution room and CPP pensionable earnings.

Reason #1 to File: Unlock “Free Money” from the Government

The Concept: Federal and provincial benefits are often “refundable” tax credits. This means you receive them even if you paid zero tax. The CRA uses your tax return to calculate these payments. No return means no money.

The GST/HST Credit

This program provides tax-free payments to low- and modest-income Albertans. For 2026, maximum amounts hit $533 for singles** and **$698 for couples, plus an extra $184 per child under 19.

The Catch: You only receive it if you file taxes in Canada in 2026. The CRA automatically calculates your eligibility based on your filed return.

The Canada Workers Benefit (CWB)

This refundable tax credit supplements earnings for low-income workers. You qualify if you:

- Earn a working income of over $3,000

- Are at least 19 years old

- Reside in Canada year-round

Income thresholds vary by province. For 2026, maximum annual amounts reach $1,633 for singles and $2,813 for families.

Alberta Child and Family Benefit (ACFB)

This provincial program supports families with children under 18. You do not need to apply separately. Filing your return triggers an automatic assessment.

2026 payment dates: February 27, May 27, August 27, November 27. Maximum benefits reach $3,746 for the base component plus $2,021 for the working component with four or more children.

Key Takeaway: Filing one return unlocks thousands in annual benefits you never directly paid for. The CRA will not pay what they cannot see.

Reason #2 to File: The CPP and the “Paper Trail”

Building Your Pension

You make contributions to the Canada Pension Plan (CPP) when you report your earnings from self-employment. For self-employed people, the contribution rate for 2026 is 11.9%.

Yes, contributing feels like a cost today. However, these payments prevent gaps in your retirement earnings history. Maximum pensionable earnings for 2026 are $74,600. Every reported dollar builds your future monthly cheque.

RRSP Room Creation

Filing generates contribution room for your Registered Retirement Savings Plan (RRSP). The calculation is simple: 18% of your earned income from the previous year, up to a maximum of $33,810 for 2026.

Skipping a filing year means losing that room permanently. Unused room carries forward, but unreported income creates no room at all.

Proof of Income (The Mortgage Test)

Calgary lenders demand proof that you exist financially. When applying for a mortgage, they require your Notice of Assessment (NOA) from the CRA.

Self-employed applicants must provide two years of tax returns and NOAs. A consistent filing history, even with low income, proves you are traceable and responsible. Banks trust paper trails.

Key Takeaway: Filing today builds tomorrow’s borrowing power and retirement security. The CRA Notice of Assessment becomes your financial passport.

The Self-Employment Deep Dive: Deductions That Matter in Calgary

Report Income, Reduce Tax: Use Form T2125 to report your business income and claim expenses. This form calculates your net income. Lower net income means lower taxes. Simple math.

I learned this the hard way. My first year freelancing, I forgot $800 in software receipts. That mistake cost me roughly $300 in extra taxes. Never again.

Top Deductions for Calgary Gig Workers

- Vehicle Expenses (The Calgary Commute): Calgary stretches from Stoney Trail to Deerfoot. If you drive for SkipTheDishes, Uber, or work in the trades, track every kilometer. Deduct gas, insurance, maintenance, and registration—but only the business portion. The CRA demands a detailed logbook. No log means no deduction.

- Home Office: Working from your Beltline apartment or Shawnessy house? Deduct a percentage of utilities, rent, internet, and maintenance. You qualify if it’s your principal place of business or if you regularly meet clients there. Calculate using square footage. Keep floor plans handy.

- Tools & Equipment: That new laptop, camera, or monitor? Deductible: Big purchases fall under Capital Cost Allowance (CCA)—you claim portions over several years. Save those receipts.

The GST/HST Nuance

If you earn under $30,000, you are a “small supplier.” You do not charge GST/HST. However, you also cannot claim Input Tax Credits (ITCs)—refunds on GST you paid for business supplies. Here is the counter-intuitive move: voluntarily register for GST/HST even below $30,000. Why? You start claiming ITCs on everything you buy. If you have high startup costs (equipment, software, vehicle), this puts cash back in your pocket. The trade-off? You must charge GST and file regularly. Run the numbers first.

Key Takeaway: Deductions turn business spending into tax savings. Track everything. Log kilometers daily. Consider voluntary GST registration if you have large expenses—it creates refunds where none existed before.

Your 2026 Calgary Tax Filing Toolkit (Step-by-Step)

Step 1: Gather Your Slips

Collect T4s (employment income), T5s (investment income), and every business expense receipt. CRA requires six years of records. Go digital now—photos beat shoeboxes.

Step 2: Know the 2026 Deadlines

- April 30, 2026: Payment deadline for taxes owed. Miss this and interest compounds daily.

- June 15, 2026: Filing deadline if you or your spouse has self-employment income

Critical distinction: pay by April 30 even if you file by June 15. The CRA separates payment from paperwork.

Step 3: Choose Your Filing Method

- Free Software: Use CRA-approved NETFILE software. Many offer free versions for simple returns.

- Community Volunteer Tax Clinic: Free tax help if you have a modest income and a simple situation. Calgary has multiple locations.

- Accountant: Worth it for complex situations, multiple income streams, or if receipts resemble confetti

Step 4: Register for “My Account”

Set up CRA My Account online.e This portal shows benefit payments, RRSP room, and your Notice of Assessment instantly. You can also track refund status and download the missing Sli.

Registration takes 10 minutes. The CRA mails a security code within 5–10 days. Do it before the tax season rush.

Key Takeaway: Winning tax season requires two things: know your deadlines (April 30 payment, June 15 filing) and register for CRA My Account now. This combination saves you from penalties and puts your financial data at your fingertips.

Conclusion

Filing your taxes isn’t just about obeying rules—it’s about claiming what’s yours. When you file taxes in Canada 2026, you unlock thousands in benefits, build RRSP room, and create a paper trail that banks and the CRA actually trust

.FAQs

1. Do I really need to file if I earned less than $30,000 from my side hustle?

Yes. The $30,000 threshold determines GST/HST registration, not filing requirements. Any amount of *self-employment income*—even $500—must be reported using Form T2125. Filing triggers the GST/HST credit, and Alberta benefits you would otherwise miss

2. What happens if I don’t file butearnd self-employment income?

The CRA already knows. Payment apps and clients report income through T4A slips. If you don’t file a return, the CRA can file a “default return” using only income data—meaning zero deductions claimed and maximum tax owed. You also lose access to refundable tax credit programs permanently for that year.

3. Can I still get the Alberta Child and Family Benefit if I file late?

Yes, but there’s a catch. You have up to 10 years to claim benefits, but payments only start after you file. The ACFB provides up to $3,746 for the base component plus $2,021 for the working component with four or more children. File now to trigger payments for the current benefit year.

4. What tax documents do I need to keep for CRA audit purposes?

Keep everything for six years: all T-slips, business expense receipts, mileage logs, and home office calculations. Digital photos of receipts stored in cloud folders satisfy CRA requirements…or vehicle expenses, detailed mileage logs tracking business versus personal kilometres are mandatory—estimates get disallowed.

5. How do I pay CPP contributions on self-employment income?

Use Schedule 8 to calculate CPP contributions based on your net self-employment income. The 2026 rate is 11.9% on earnings between $3,500 and $74,600. Half is tax-deductible. If you also have T4 employment income, the CRA coordinates both to prevent overpayment.